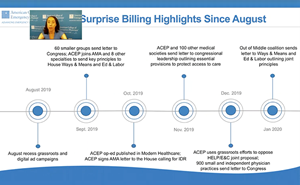

The health policy community got a special gift right before the start of the July Fourth weekend. Last Thursday, July 1st, the Departments of Health and Human Services (HHS), Treasury, and Labor (referred to as “the Departments” throughout) issued an interim final regulation (IFR) implementing part of the No Surprises Act. The No Surprises Act, which Congress passed at the end of last year, bans balance billing for out-of-network (OON) services starting in 2022 and establishes a back-stop independent dispute resolution (IDR) process to ensure that clinicians and facilities are paid appropriately for the OON services they deliver.

Background

For the last two years, ACEP has advocated on behalf of you as emergency physicians and your patients to ensure that any legislation that would address surprise medical billing would truly keep patients out of the middle of billing disputes and include a fair payment mechanism that would hold health care plans accountable and ensure adequate reimbursement for OON services. We ultimately believe that the No Surprises Act represents a mostly reasonable solution to this issue given how damaging initial Congressional proposals would have been for emergency physicians.

After the No Surprises Act was passed last December, we teamed up with the Emergency Department Practice Management Association (EDPMA) to form a joint task force that represented the whole house of emergency medicine (EM). As a task force, we were able to engage directly with key federal agencies in charge of implementing the law—even before any regs were released. In March, we sent a 19-page letter outlining our policy positions on key issues that affect emergency care, and in May, we followed-up with another letter that provided technical feedback on the specific information that will be necessary to accurately bill patients for OON emergency services. Further, we met directly with the federal government several times in June—including an informal meeting with the Center for Consumer Information and Insurance Oversight (CCIIO)—the main agency implementing the law—and an official meeting with the White House’s Office of Management and Budget.

Although we did a lot of “pre-work,” the IFR itself represents the official starting point of the implementation process. It focuses on some major issues that impact how much patients will pay for OON emergency care and certain OON non-emergency services. It also includes definitions for key terms that will affect the amount clinicians and facilities will receive from health care plans for OON services. However, the IFR does not touch upon some extremely important policies, including the IDR process—which, in some cases, will actually determine the ultimate payment that a clinician or facility will receive for an OON service. Another IFR that will focus on these other issues is expected later this summer or early fall.

Comments on the first IFR are due on September 7, 2021. Rest assured, ACEP and EDPMA plan to submit a comprehensive response to the reg.

Details of the IFR

ACEP has created a comprehensive summary of the IFR, but I wanted to present you with some highlights and perspective. Also, to give you all a heads up, you should expect to see some future regs and eggs blogs that dive deeper into certain topics.

It is important to note that federal agencies are not implementing the No Surprises Act through the traditional regulatory process. Usually, federal agencies release a proposed reg and then a final reg after a 30- or 60-day public comment period. However, this reg is an “interim final reg” with comment period. Although the Departments must eventually issue a final reg based on public comments, the policies included in this reg are considered final (and not just proposed) in the interim. As a rationale for why the Departments are issuing an interim final reg instead of a proposed reg, they explain in the IFR how they wanted to allow enough time before January 1, 2022 for all stakeholders—health care plans, patients, and clinicians—to understand and implement the requirements. Finally, the No Surprises Act requires the Departments to issue regulations on certain topics by July 1, 2021, and the Departments stated that they simply didn’t have enough time to go through the full regulatory process prior to that date.

Prudent Layperson Standard

One significant victory for both you and your patients is that the IFR strongly re-enforces the prudent layperson standard. The prudent layperson standard allows people who reasonably think they are having an emergency to come to the emergency department (ED) without worrying about whether the services they receive will be covered by their insurance. Under the prudent layperson standard, health insurers cannot deny reimbursement to clinicians based on the patient’s final diagnosis. An “emergency” versus a “non-emergency” must be determined on a case-by-case basis based on whether the patient’s symptoms and complaints reasonably represented to them as a prudent layperson a potential emergency condition.

While that’s what the prudent layperson standard states, that’s not what some insurance companies are actually doing. For example, UnitedHealthcare recently announced a policy to retroactively deny patients’ emergency care claims. Although UnitedHealthcare quickly decided to temporarily delay its implementation due to a swift backlash (ACEP led the way on that advocacy effort), United still plans to implement the policy eventually. Fortunately, the IFR addresses these bad payor practices directly and explicitly states that these practices are inconsistent with the emergency services requirements of the No Surprises Act and the Affordable Care Act. The IFR also emphasizes that the determination of whether the prudent layperson standard is met must be made be before an initial denial of an emergency services claim.

Downcoding

Although the prudent layperson standard language in the IFR directly addresses the issue of denying care, it does not explicitly refer to another inappropriate practice many health care plans are implementing—downcoding. If claims are downcoded by health insurers, the services are still covered by the insurers (rather than denied), but the level of service on the claim is changed. Emergency physicians typically bill the ED evaluation and management (E/M) codes (Current Procedural Terminology [CPT] codes 99281-99285). An example of a claim downcoded by a payor is the scenario where an emergency physician bills a CPT code 99285 (a level 5 service), but the payor adjusts the code on the claim to a CPT code 99284 (a level 4 service). ACEP and EDPMA have strongly pushed back against downcoding policies, arguing that there are clear documentation standards and guidelines that dictate what level of service should be included on the claim. We had asked federal agencies to directly call out downcoding as a prudent layperson standard violation if health insurers retroactively adjust the CPT code(s) found on the claim based on a review of the final diagnosis.

Qualifying Payment Amount

The issue of downcoding also indirectly comes up in the context of the “qualifying payment amount” (QPA). Under the No Surprises Act, the QPA is used for two purposes:

- To determine cost-sharing requirements for patients if an all-payer model or specified state law does not apply (more on specified state laws later…) and;

- As a factor that IDR entities can consider in order to determine the total payment for OON emergency services.

The law defines QPA as the median of the contracted rates recognized by the plan on January 31, 2019, for the same or similar service that is provided by a provider in the same or similar specialty and provided in a geographic region in which the service is furnished (increased for inflation). The IFR goes into detail about each of these different factors:

- How the median contracted rate is determined and updated by inflation;

- How “insurance market” is defined;

- What a “same or similar item or service” means;

- How health care plans should take into account services delivered by a provider with the “same or similar specialty;”

- How to define geographic regions;

- How to take into account “non-fee-for-service contractual arrangements”; and,

- How to calculate the QPA in cases where the health care plan has insufficient information to do so.

With respect to “same or similar item or service,” ACEP and EDPMA had asked CCIIO and other federal agencies to require health care plans to base the QPA on the specific CPT code(s) that is included on the initial claim—in part to address the underlying issue of downcoding. If health care plans can base the QPA on a CPT code that they think should be attributed to the service delivered—not necessarily the CPT code on the claim itself—then that could keep the door open for them to continue downcoding claims. For example, if a clinician bills an ED E/M level 5 service code (CPT 99285), a health care plan could have the flexibility to choose a QPA based on an ED E/M level 4 service code (CPT 99284) instead. Remember, the QPA is a factor that the IDR entity must consider, so the selection of the QPA could impact the final OON payment a clinician or facility receives. Although the IFR would require health care plans to base the QPA on the specific CPT code for the service delivered, unfortunately it does not include the explicit reference to the “CPT code on the claim” that we requested. While that is disappointing, we hope that federal agencies will dive more into this issue of downcoding in the next IFR that focuses on the IDR process.

Specified State Laws

Moving on, another issue in the IFR is how the Departments choose to define a “specified state law.” As alluded to earlier, the No Surprises Act establishes a federal methodology for calculating the cost-sharing amount (the QPA) as well as the total payment a clinician or facility receives for OON emergency services and certain non-emergency services. However, the No Surprises Act says that if states already have a law in place that protects patients from balance billing and that includes a method for determining the cost-sharing amount and payment amount for OON services, then that state approach should be used instead of the federal methodology. In the IFR, the Departments state that in order for the state law to be used, it must apply to the health care plan involved, the OON clinician or facility involved, and the service involved. If a state law does not satisfy all these criteria, it would not apply. For example, if the state law did not apply to emergency services, but did apply to certain non-emergency services, the federal law would be used to determine the cost-sharing amount and OON rate for emergency services while the state law would be used to determine the cost-sharing amount and OON rate for certain non-emergency services. While this process for determining whether a state law applies appears to be clear, there are definitely ambiguous cases that may require further guidance (such as states that determine the cost-sharing amount and OON rate only for claims above a certain dollar threshold).

In addition, the Departments seem to make a conscious effort to widen the applicability of state laws in the IFR by including a very broad definition of what counts as a method of determining the total amount payable for OON services. The IFR allows certain plans that aren’t traditionally subject to state laws—i.e., self-insured plans, also known as Employee Retirement Income Security Act (ERISA) plan—to voluntarily opt-in to using the state’s methodology. Beyond just ERISA plans, the Departments also seek comment on whether any health insurers, clinicians, or facilities who are not subject to state law can opt into a program established under state law, including on an episodic basis. If the Departments ultimately go down that road—allowing any clinician, facility, or health care plan to opt into a state law (even on a case-by-case basis)—then they would truly be leading us on the path towards the wild, wild west in the health care insurance market. The Departments even recognize that such an approach could increase health care prices if clinicians and facilities selectively opt in to state programs that favor clinicians and facilities in the determination of the OON rate.

Initial Payment

The IFR also fleshes out requirements around an initial payment or denial that the health care plan must make to a OON clinician or facility within 30 calendar days after the clinician or facility submits a bill and the health care plan receives the claim. The IFR refers to a “clean claim,” which means that the claim includes all the information needed for the health care plan to process the claim. Fortunately, the Departments recognize that insurers could try to delay the initial payment by asserting that they did not receive a clean claim, and therefore the IFR states that the Departments may specify additional standards if they become aware of instances of abuse and gaming.

With respect to an initial payment, the Departments don’t think that it should be a first installment of a final payment, but instead should reflect the insurer’s best effort to make a full payment. In other words, health care plans can’t just initially pay you $1 for an OON service and wait for the negotiation and IDR processes to play out before paying you an appropriate amount. The IFR does not require the insurer to make a minimum amount of initial payment, but the Departments are seeking comment on whether to set a minimum payment rate or methodology for a minimum initial payment, and if so, what that rate or methodology should be. A major potential downside to a minimum initial payment is that, if a rate or methodology is ultimately adopted, it could become the de-facto payment amount for an OON service. ACEP and EDPMA had opposed early congressional efforts to create a benchmarking approach to setting OON payment rates—and adding a minimum payment amount requirement could lead us in that direction.

Resolving Disputes

The IFR also provides some clarifications on the type of disputes that can go through an insurer’s traditional appeals process, and which can go through the No Surprises Act negotiations and IDR processes. Overall, when the patient’s cost-sharing is involved, a dispute can go through the plan’s traditional appeals process. When the patient is not involved, and the dispute just involves the payment between the health care plan and the clinician or facility, it can go through the No Surprises Act negotiation and IDR processes. Interestingly, the Departments acknowledge there may be instances where patients appeal their cost-sharing amount through the claims and appeals process concurrently with a clinician’s challenge to a payment amount through the IDR process. Trying to figure out the appropriate cost-sharing amount and final payment amount at the same time could be very confusing for all parties involved.

Other Policies in the IFR

There are numerous other policies in the IFR, including a notice and consent process that will allow clinicians to balance bill patients for certain non-emergency services (e.g., if a patient has a scheduled surgery, the patient can agree ahead of time to have an OON surgeon perform the surgery and receive a balance bill for that service). The reg also establishes an auditing process and includes details around how the Departments plan to enforce the requirements. Finally, the IFR requires clinicians and facilities to provide public disclosures regarding patient protections against balance billing.

As I mentioned earlier, I may dive deeper into some of these policies (and how ACEP and EDPMA plan to respond to them during the public comment period) in future regs and eggs blogs—so, stay tuned!

Until next week, this is Jeffrey saying, enjoy reading regs with your eggs.